As we wrap up the 2016 harvest, wineries and growers begin to settle up for grape deliveries. What determines grape pricing and how does this pricing affect wine pricing?

As we wrap up the 2016 harvest, wineries and growers begin to settle up for grape deliveries. What determines grape pricing and how does this pricing affect wine pricing?

Because Napa grape costs are the highest in California, virtually all red wine made with Napa grapes must be retail priced at $40 or more per bottle for the winery to receive a reasonable profit. The majority of Napa’s production is from two Bordeaux varieties, Cabernet Sauvignon (43%) and Merlot (11%). When the other three Bordeaux varieties, Cab Franc, Malbec and Petit Verdot are added, production totals 59% of Napa’s grape crop.

Napa’s lower priced grapes are dominated by white varieties, Chardonnay and Sauvignon Blanc, representing approximately 25% of Napa production.

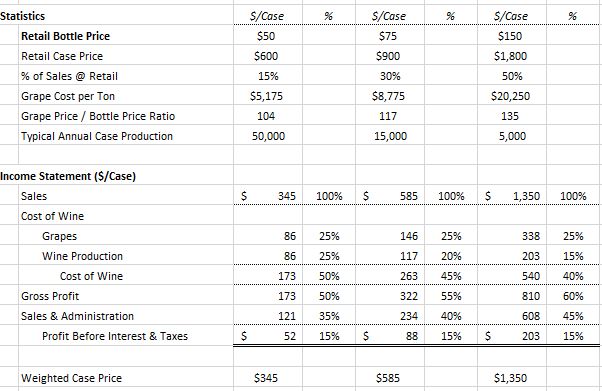

Since Cabernet Sauvignon is the dominant variety in Napa, let’s focus on the economics of its production and pricing. For a winery to experience a reasonable profit, grape costs should not exceed 25% of the wine’s selling price. As a consequence, the tonnage grape to retail bottle price ratio should range from 100 for lower priced Napa Cabernet Sauvignon to as high as 140 times for more expensive Cabernet.

The attached winery profiles show the economics at various wine pricing levels. In each of these profiles, the winery realizes a profit equal to 15% of sales. Most Napa Valley wineries sell a mix of retail and wholesale through distributors. Traditionally, sales to distributors are at 50% of the retail price. As the wine price goes up, generally a higher portion of wine is sold retail, so while wine production costs increase in absolute terms, they will decrease as a percentage of sales. Offsetting this increased gross profit are higher selling and administrative costs per case due to the combination of lower sales volume, a higher percentage of retail sales and a lack of scale.

Bottom line, if Napa Valley wine is retail priced outside of this 100 to 140 times grape cost to bottle price range, the economics don’t work for the winery.

Bubbly, Champers, Sparklers, Fizz – when consumers are looking for sparkling wine, they are no longer simply being offered French Champagne. Other country’s products, like Italian Prosecco, Spanish Cava and US Méthode Champenoise are flooding the market.

Bubbly, Champers, Sparklers, Fizz – when consumers are looking for sparkling wine, they are no longer simply being offered French Champagne. Other country’s products, like Italian Prosecco, Spanish Cava and US Méthode Champenoise are flooding the market. Not only is more sparkling wine being made – more wine is being drunk.

Not only is more sparkling wine being made – more wine is being drunk. For producers & winemakers, there are some barriers to entrance in this market – most notably production costs (especially for Méthode Champenoise) & global competition but sparkling wine lovers now have more options by price point, style of wine and country of origin than ever before. Cheers to that.

For producers & winemakers, there are some barriers to entrance in this market – most notably production costs (especially for Méthode Champenoise) & global competition but sparkling wine lovers now have more options by price point, style of wine and country of origin than ever before. Cheers to that.